PERSONAL - Applied Regression

Recap: Basic Statistics

- mean (expected value): the

mean of the possible values a random variable can take

- notation: E(X) = \mu

- finitely many outcomes: E(X) = x_1p_1 + ... + x_np_n

- countably infinitely many outcomes: E(X) = \sum_{i=1}^\infty x_ip_i

- random variables with density: E(X) = \int_{-\infty}^\infty xf(x)dx

- properties:

- E(c) = c

- E(aX + b) = aE(x) + b

- E(a_1X_1 + ... + a_nX_n) = a_1E(X_1) + ... + a_nE(X_n)

- E(X_1 \cdot ... \cdot X_n) = E(X_1) \cdot ... \cdot E(X_n) for independent (uncorrelated) X_i

- E(g(X)) = \int_\R g(x)f(x)dx

- notation: E(X) = \mu

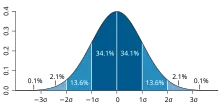

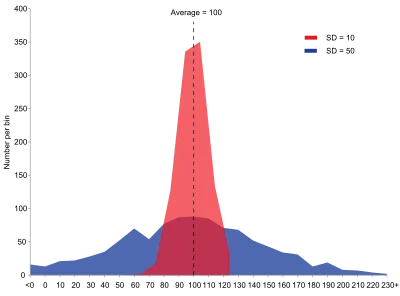

- standard deviation: a

measure of the amount of variation of the values of a variable about its mean

- definition: \sigma = \sqrt{Var(X)}

- standard error: the

standard deviation of its sampling distribution or an estimate of that standard deviation

- definition: se = \frac{\sigma}{\sqrt{n}} for n observations

- variance: a measure of how far a

set of numbers is spread out from their average value

- notation: Var(X) = \sigma^2

- definition: Var(X) = E(X^2) - E(X)^2

- properties:

- Var(c) = 0

- Var(X + a) = Var(X)

- Var(aX) = a^2Var(X)

- Var(aX \pm bY) = a^2Var(X) + b^2Var(Y) \pm 2ab\;Cov(X,Y)

- Var(X_1 + ... + X_n) = Var(X_1) + ... + Var(X_n) for independent (uncorrelated) X_i

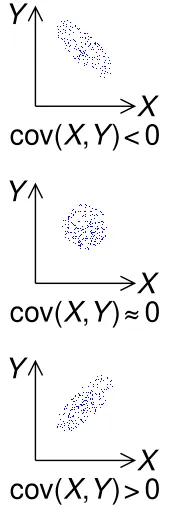

- covariance: a measure of the

joint variability of two random variables

- definition: Cov(X,Y) = E(XY) - E(X)E(Y)

- positively correlated variables: Cov(X,Y) > 0

- negatively correlated variables: Cov(X,Y) < 0

- uncorrelated variables: Cov(X,Y) = 0 (but not the other way

around!)

- independent variables: Cov(X,Y) = 0

- properties:

- Cov(X,X) = Var(X)

- Cov(X,Y) = Cov(Y,X)

- Cov(X,c) = 0

- Cov(aX, bY) = ab\;Cov(X,Y)

- Cov(X+a, Y+b) = Cov(X,Y)

- Cov(aX + bY, cW + dV) = acCov(X,W)+adCov(X,V)+bcCov(Y,W)+bdCov(Y,V)

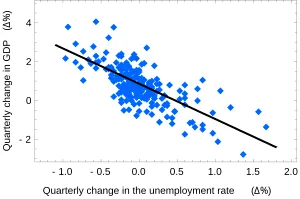

- correlation: any statistical

relationship, whether causal or not, between two random variables

- definition: Corr(X,Y) = \frac{Cov(X,Y)}{\sqrt{Var(X)Var(Y)}}

Introduction

- regression: creates a functional relationship between a response

(dependent) variable and a set of explanatory (predictor) variables

(covariates)

- regression model: which explanatory variables have an effect on the response?

- deterministic relationship: a certain input will always lead to the same result

- parameter: an unknown constant, most likely to be estimated by collecting and using data

- empirical model: any kind of model based on empirical observations rather than on mathematically describable (theory-based) relationships of the system modelled

- controlled experiment: one where the experimenter can set the values of the explanatory variable(s)

- line definition (linear model): y = \beta_0 + \beta_1 x ( + \epsilon )

- \beta_0,

\beta_1:

constants (parameters)

- intercept \beta_0: y when x = 0

- slope \beta_1: change in y if x is increased by 1 unit

- \epsilon: random

disturbance (error)

- \beta_0 + \beta_1 x: deterministic

- \epsilon: random, models variability in measurements around the regression line

- linear in \beta_0 and \beta_1

- for each experiment: y_i = \beta_0 + \beta_1 x_i + \epsilon_i

- input and result: (x_i, y_i)

- \beta_0, \beta_1 remain constant

- x_i, \epsilon_i

vary per experiment i = 1,2,...,n

- mean E(\epsilon_i) = 0

- variance Var(\epsilon_i) = \sigma^2

- \epsilon_i, \epsilon_j independent random variables for i \neq j

- x_i deterministic (i.e. the input data is clearly and certainly defined; it can also be noisy, in which case x_i is not deterministic)

- \implies y_i

random variable; y_i, y_j

independent for i \neq j

- mean E(y_i) = E(\beta_0 + \beta_1 x_i + \epsilon_i) = \beta_0 + \beta_1 x_i + \underbrace{E(\epsilon_i)}_0 = \beta_0 + \beta_1 x_i

- variance Var(y_i) = \sigma^2

- unexplained variability \sigma

- general: y = \mu + \epsilon

- deterministic component \mu = \beta_0 +

\beta_1 x_1 + ... + \beta_p x_p

- explanatory variables x_1, ... , x_p (assume fixed, measured without error)

- \beta_i, i = 1,2,...,p: change in \mu when changing x_i by one unit while keeping all other explanatory variables the same

- E(y) = \mu, Var(y) = \sigma^2

- deterministic component \mu = \beta_0 +

\beta_1 x_1 + ... + \beta_p x_p

- linearity: the derivatives of \mu with respect to the parameters \beta_i do not depend on the variables

- \beta_0,

\beta_1:

constants (parameters)

- notation: x_{ij}

for the i-th unit (i.e. row

in a table) and the j-th

explanatory variable (i.e. column in a table) (R:

table[i,j]) - dependent variable: depends on an independent variable

Simple Linear Regression

- simple linear regression

model: y =

\mu + \epsilon

- mean E(y) = \mu = \beta_0 + \beta_1 x

- one predictor (regressor) variable x

- one response variable y

- random error \epsilon

- for n pairs of

observations (x_i, y_i): y_i = \beta_0 + \beta_1 x_i

+ \epsilon_i,\;\; i = 1, ..., n

- x_i not random (can be selected by experimenter)

- \epsilon_i \sim N(0, \sigma^2)

- y_i \sim N(\mu_i, \sigma^2), where \mu_i = \beta_0 + \beta_1 x_i

- E(\epsilon_i) = 0

- E(y_i) = \mu_i = \beta_0 + \beta_1 x_i

- Var(\epsilon_i) = \sigma^2

- Var(y_i) = \sigma^2

- Cov(\epsilon_i, \epsilon_j) = 0 for i \neq

j

- any two observations y_i, y_j are independent for i \neq j

- goal: estimate \beta_0, \beta_1, \sigma^2

from available data (x_i, y_i)

- zero slope \implies absence of linear association

- unbiased parameter estimate: E(\hat\theta) = \theta

- biased parameter estimate: E(\hat\theta) \neq \theta

- least squares estimation

(LSE): a mathematical procedure for finding the best-fitting curve to a

given set of points by minimizing the sum of the squares of the offsets ("the

residuals") of the points from the curve

- goal: minimize \sum_{i=1}^n (y_i - \hat y_i)^2

where \hat y_i = \hat \beta_0 +

\hat \beta_1 x_i

(fitted value)

- LSE \hat \beta_1 = \frac{\sum_{i=1}^n (x_i -

\overline x)(y_i - \overline y)}{\sum_{i=1}^n (x_i - \overline x)^2} =

\frac{s_{xy}}{s_{xx}}

- s_{xy} = \sum_{i=1}^n (x_i - \overline x)(y_i - \overline y)

- s_{xx} = \sum_{i=1}^n (x_i - \overline x)(x_i - \overline x)

- (!) reordering using \sum_{i=1}^n (x_i - \overline x) =

0:

- \hat \beta_1 = \frac{\sum_{i=1}^n (x_i - \overline x) y_i}{\sum_{i=1}^n (x_i - \overline x)^2}

- s_{xx} = \sum_{i=1}^n x_i(x_i - \overline x)

- LSE \hat \beta_0 = \overline y - \hat \beta_1 \overline x

- LSE s^2 = \frac1{n-2}\sum_{i=1}^n (y_i - \hat

y_i)^2

- short: s^2 = \frac{\sum_{i=1}^n e_i^2}{n-2}

- residual e_i = y_i - \hat y_i

- degree of freedom: number of independent observations (n) minus the number of estimated parameters (here 2, \beta_0 and \beta_1)

- sample mean \overline x = \frac1n\sum_{i=1}^n x_i

- result mean \overline y =

\frac1n\sum_{i=1}^n y_i

- \overline y = \hat\beta_0 + \hat\beta_1 \overline x

- E(\hat \beta_1) = \beta_1

- E(\hat \beta_0) = \beta_0

- E(\overline y) = \beta_0 + \beta_1 \overline x

- E(s^2) = \sigma^2

- Var(\hat \beta_1) = \frac{\sigma^2}{s_{xx}}

- Var(\hat \beta_0) = \sigma^2\left(\frac1n + \frac{\overline x^2}{s_{xx}}\right)

- se(\hat \beta_1) = \frac{s}{\sqrt{s_{xx}}}

- LSE \hat \beta_1 = \frac{\sum_{i=1}^n (x_i -

\overline x)(y_i - \overline y)}{\sum_{i=1}^n (x_i - \overline x)^2} =

\frac{s_{xy}}{s_{xx}}

- goal: minimize \sum_{i=1}^n (y_i - \hat y_i)^2

where \hat y_i = \hat \beta_0 +

\hat \beta_1 x_i

(fitted value)

- maximum likelihood

estimation (MLE): a method of estimating the parameters of an assumed

probability distribution by maximizing a likelihood function

- \hat \sigma^2 = \frac1n\sum_{i=1}^n(y_i - \hat y_i)^2 (biased!)

- null hypothesis

testing: a method of statistical inference used to decide whether the data

sufficiently supports a particular hypothesis

- t-test:

a statistical test used to test whether the difference between the response of two groups is

statistically significant or not (here: two-sided)

- H_0: \beta_1 = 0 vs. H_A: \beta_1 \neq 0 (\leq or >)

- T = \frac{\hat \beta_1}{se(\hat \beta_1)} \sim t_{n-2}

- \alpha

usually 0.05

- quantile approach: reject H_0 if |T| > t_{n-2, 1-\alpha /2}

- probability approach: reject H_0

if p-value

is less than \alpha

- p-value:

the probability of obtaining test results at least as extreme as the

result actually observed, under the assumption that the null

hypothesis is correct

- R:

2 * pt(abs(tval), df, lower.tail = FALSE)

- R:

- the lower the p-value, the more far-fetched the null hypothesis is

- p-value:

the probability of obtaining test results at least as extreme as the

result actually observed, under the assumption that the null

hypothesis is correct

- t-test:

a statistical test used to test whether the difference between the response of two groups is

statistically significant or not (here: two-sided)

- confidence interval:

an interval which is expected to typically contain the parameter being estimated

- 100(1-\alpha)\% confidence

interval for \beta_1:

\hat \beta_1 \pm t_{n-2,

1-\alpha/2} \cdot se(\hat\beta_1)

- general: \text{Estimate ± (t value)(standard error of estimate)}

- 100(1-\alpha)\% confidence

interval for \beta_1:

\hat \beta_1 \pm t_{n-2,

1-\alpha/2} \cdot se(\hat\beta_1)

- prediction of a new point: y_p = \hat \beta_0 + \hat \beta_1 x + \epsilon, where \epsilon \sim N(0, \sigma^2)

- analysis of variance (ANOVA): a collection of statistical models and their

associated estimation procedures used to analyze the differences between groups

- SST = SSR + SSE

| Source | d.f. | SS (Sum of Squares) | MS (Mean Square) | F |

|---|---|---|---|---|

| Regression | 1 | SSR=\sum_{i=1}^n(\hat y_i - \overline y)^2 | MSR = SSR | \frac{MSR}{MSE} |

| Residual (Error) | n-2 | SSE=\sum_{i=1}^n(y_i - \hat y_i)^2 | MSE = s^2 | |

| Total | n-1 | SST=\sum_{i=1}^n(y_i - \overline y)^2 |

- F-test: any statistical test used

to compare the variances of two samples or the ratio of variances between multiple samples

- H_0: \beta_1 = 0 vs. H_A: \beta_1 \neq 0

- T \sim t_v \implies T^2 \sim F_{1,v}

- quantile approach: reject H_0

if F >

F_{1,n-2,1-\alpha}

(

qf(1 - alpha, 1, n - 2)) - probability approach: reject H_0 if P(f > F) < \alpha where f \sim F_{1,n-2}

- coefficient of

determination: the proportion of the variation in the dependent variable that

is predictable from the independent variable(s)

- R^2 = \frac{SSR}{SST} = 1 -

\frac{SSE}{SST}

- interpretation: 100 R^2 \% of the variation in y can be explained by x

- 0 \leq R^2 \leq

1

- the better the linear regression (right) fits the data in comparison to the simple average (left), the closer the value of R^2 is to 1

- R^2 = \frac{SSR}{SST} = 1 -

\frac{SSE}{SST}

- Pearson

correlation: a correlation coefficient that measures linear

(!) correlation between two variables x,y

- r = \text{sign}(\hat \beta_1) \sqrt{R^2}

- in R...

cov(x,y)returns \frac1{n-1}\sum_{i=1}^n(x_i-\overline x)(y_i - \overline y)var(x)returns \frac1{n-1}\sum_{i=1}^n(x_i-\overline x)^2cor(x,y)returns \frac{Cov(x,y)}{sd(x)sd(y)}sd(x)returnssqrt(var(x))

- diagnostics: y \sim

N(\beta_0 + \beta_1 x, \sigma^2)

- independence: told by investigator

- linearity: plot y against x

- constant variance: plot y-\hat y against \hat y

- normal distribution: plot y - \hat y against normal quantiles

Recap: Matrix Algebra

- matrix: a rectangular

array of numbers

- formally: A \in p \times q

(matrix A with p rows and

q

columns)

- A = (a_{ij}), where {a_{ij}} is the entry in row i and column j

- square matrix: same number of rows and columns (p=q)

- det(AB) = det(A)det(B) (also written as |AB| = |A||B|)

- identity matrix I: square matrix with ones in the diagonal and zeros everywhere else

- zero matrix O: matrix of all zeros

- diagonal (square) matrix: all entries outside the diagonal are zero

- formally: A \in p \times q

(matrix A with p rows and

q

columns)

- (column) vector: a

matrix consisting of a single column

- formally: \boldsymbol{x} \in p \times 1

- \boldsymbol{x} = (x_i)

- elements: x_1, ... , x_p

- unit vector \boldsymbol{1}: vector with all elements equal to one

- zero vector \boldsymbol{0}: vector with all elements equal to zero

- formally: \boldsymbol{x} \in p \times 1

Operations and Special Types

- matrix / vector addition: element-wise, same dimensions

- matrix / vector multiplication: for A \in p \times q,\;\;B \in q \times t, go through each

row in the first matrix and multiply and add the elements with the elements of each column in the

second matrix; that's one complete row in the result matrix

- formally: C = AB = (c_{ij}) \in p \times t with c_{ij} = \sum_{r=1}^q a_{ir}b_{rj}

- (AB)C = A(BC)

- (A+B)C = AC + BC

- A(B+C) = AB+AC

- matrix transposition: interchange rows and columns

- formally: A' = (a_{ji}) with A \in q \times p

- symmetric matrix: A = A'

- (A+B)' = A' + B'

- (A')' = A

- (cA)' = cA'

- (AB)' = B'A' for A \in m \times n, B \in n \times p

- (inner) vector product: multiply element-wise, then add all together \to scalar

- formally: \boldsymbol{x'y} = \sum_{i = 1}^p x_iy_i

- orthogonal vectors: inner product 0

- euclidian norm (length): || \boldsymbol{x}|| = \sqrt{\boldsymbol{x'x}}

- set of linearly dependent vectors: there exist scalars c_i,

not all simultaneously zero, such that c_1\boldsymbol{x_1} + ... + c_k\boldsymbol{x_k} = 0

- (!) at least one vector can be written as a linear combination of the remaining ones (for example, a column in a matrix is the summation of two other columns)

- linearly independent: otherwise

- matrix rank: largest number of linearly independent columns (or rows)

- nonsingular matrix: square matrix with rank equal to row / column number

- formally: A \in m\times m, \; \; {rank}(A) = m

- nonsingular matrix: square matrix with rank equal to row / column number

- matrix inverse: AA^{-1} = A^{-1}A = I

- ABB^{-1}A^{-1} = I

- (A^{-1})' = (A')^{-1}

- (\lambda A)^{-1} = \frac1\lambda A^{-1}

- for nonsingular matrices: (AB)^{-1} = B^{-1}A^{-1}

- orthogonal (square) matrix: AA' = A'A = I

- A' = A^{-1}

- the rows (columns) are mutually orthogonal

- the length of the rows (columns) is one

- det(A) = \pm 1

- trace of a (square) matrix: the sum of its diagonal elements

- formally: tr(A) = \sum_{i=1}^m a_{ii}

- tr(A) = tr(A')

- tr(A+B) = tr(A) + tr(B)

- tr(CDE) = tr(ECD) = tr(DEC) for conformable matrices C,D,E (matrices s.t. products are defined)

- tr(c) = c

- bonus: E(tr(\cdot)) = tr(E(\cdot))

- idempotent (square) matrix: AA = A

- det(A) = 0 or 1

- rank(A) = tr(A)

Simple Regression (Matrix)

- simple regression (matrix approach): \boldsymbol{y = X\beta + \epsilon}

- \boldsymbol{y, \epsilon} are (n \times 1) random vectors

- \boldsymbol X is a (n \times 2) matrix (first col. ones, second column x_i

- LSE \boldsymbol{\hat \beta = (X'X)^{-1}X'y}

- fitted value vector \boldsymbol{\hat y = X \hat \beta}

- residual vector \boldsymbol{e = y - \hat y = y - X \hat \beta}

- LSE s^2 = \frac1{n-2}\boldsymbol{e'e}

- random vector: vector \boldsymbol y

of random variables

- mean (expected value) E(\boldsymbol y) = (E(y_1), ..., E(y_n))' = \boldsymbol

\mu

(non-random vector)

- E(y_i) = \mu_i

- for a random matrix: E(Y) = \begin{pmatrix} E(y_{11}) & \dots & E(y_{1n})\\\vdots & \ddots & \vdots \\ E(y_{n1}) & \dots & E(y_{nn}) \end{pmatrix} (non-random matrix)

- properties: a scalar

constant, \boldsymbol b

vector of constants, \boldsymbol y

random vector, A matrix of

constants...

- E(a\boldsymbol{y + b}) = aE(\boldsymbol y) + \boldsymbol b

- E(A \boldsymbol y) = A \; E(\boldsymbol y)

- E(\boldsymbol y' A) = E(\boldsymbol y)' A

- Var(A \boldsymbol y) = A \:Var(\boldsymbol y)A'

- if \boldsymbol y is normal distributed, so is A \boldsymbol y

- mean (expected value) E(\boldsymbol y) = (E(y_1), ..., E(y_n))' = \boldsymbol

\mu

(non-random vector)

- covariance matrix \Sigma: diagonal

elements Var(y_i), off-diagonal elements Cov(y_i, y_j)

- formally: Var(Y) = \Sigma = \begin{pmatrix}E((y_1 - \mu_1)(y_1 - \mu_1)) & \dots & E((y_1 - \mu_1)(y_n - \mu_n)) \\ \vdots & \ddots & \vdots \\ E((y_n - \mu_n)(y_1 - \mu_1)) & \dots & E((y_n - \mu_n)(y_n - \mu_n))\end{pmatrix} = E((\boldsymbol{y-\mu})(\boldsymbol{y-\mu})')

- \Sigma symmetric, because Cov(y_i, y_j) = Cov(y_j, y_i)

- \Sigma diagonal if observations (y_i) are independent, because Cov(y_i, y_j) = 0, i \neq j

Multiple Regression

- general linear model: y =

\beta_0 + \beta_1 x_1 + ... + \beta_p x_p + \epsilon

- response variable y

- several independent (predictor, explanatory) variables x_i

- n cases,

p

predictor values: y_i = \beta_0 + \beta_1x_{i1} + ... + \beta_p x_{ip} +

\epsilon_i = \mu_i + \epsilon_i

- x_{ij}: value of the j-th predictor variable of the i-th case

- y_1, ..., y_n iid., normal distributed, y_i \sim N(\mu_i, \sigma^2)

- \mu_i non-random (deterministic)

- E(\epsilon_i) = 0

- E(y_i) = \mu_i = \beta_0 + \beta_1 x_{i1} + ... + \beta_p x_{ip}

- Var(\epsilon_i) = \sigma^2

- Var(y_i) = \sigma^2

- vector form: \boldsymbol y = X \boldsymbol \beta + \boldsymbol

\epsilon

- \boldsymbol y = \begin{pmatrix}y_1 \\ \vdots \\ y_n\end{pmatrix}, \boldsymbol y \sim N(X \boldsymbol \beta, \sigma^2 I), E(\boldsymbol y) = X \boldsymbol \beta, Var(\boldsymbol y) = \sigma^2I

- X = \begin{pmatrix} 1 & x_{11} & \dots & x_{1p} \\ \vdots & \vdots & \ddots & \vdots \\ 1 & x_{n1} & \dots& x_{np} \end{pmatrix} fixed, non-random, full rank

- \boldsymbol \beta = \begin{pmatrix}\beta_0 \\ \vdots \\ \beta_p\end{pmatrix}

- \boldsymbol \epsilon = \begin{pmatrix}\epsilon_1 \\ \vdots \\ \epsilon_n\end{pmatrix}, \boldsymbol \epsilon \sim N(\boldsymbol 0, \sigma^2 I), E(\boldsymbol \epsilon) = \boldsymbol 0, Var(\boldsymbol \epsilon) = \sigma^2I

- LSE: \boldsymbol{\hat\beta} = (X'X)^{-1}X'\boldsymbol y

- fitted values \boldsymbol{\hat y} = X\boldsymbol{\hat \beta} =

H\boldsymbol y

- H = X(X'X)^{-1}X' \in n \times n

- H is the orthogonal projection of \boldsymbol y onto the linear space spanned by column vectors of X

- H symmetric (H' = H)

- H idempotent (HH = H)

- E(\boldsymbol{\hat y}) = X \boldsymbol \beta

- Var(\boldsymbol{\hat y}) = \sigma^2 H

- H = X(X'X)^{-1}X' \in n \times n

- residuals \boldsymbol e = \boldsymbol y - \boldsymbol{\hat y} =

(I-H)\boldsymbol y

- (I-H) projects \boldsymbol y onto the perpendicular space to the linear space spanned by the column vectors of X

- (I-H) symmetric ((I-H)' = (I-H))

- (I-H) idempotent ((I-H)(I-H) = (I-H))

- rearranged: \boldsymbol y = \boldsymbol{\hat y} + \boldsymbol e = H\boldsymbol y + (I-H) \boldsymbol y

- E(\boldsymbol e) = \boldsymbol 0

- Var(\boldsymbol e) = \sigma^2(I-H)

- E(\boldsymbol{\hat \beta})

= \boldsymbol \beta

- E(\hat \beta_i) = \beta_i

- Var(\boldsymbol{\hat

\beta}) = \sigma^2(X'X)^{-1}

- Var(\hat \beta_i) = \sigma^2 v_{ii}, where v_{ii} is the corresponding diag. el. in (X'X)^{-1}

- fitted values \boldsymbol{\hat y} = X\boldsymbol{\hat \beta} =

H\boldsymbol y

- MLE: s^2 = \frac{SSE}{n-k-1} = \frac1{n-k-1}\sum_{i=1}^n(y_i - \hat y_i)^2 (for k predictors not including the intercept!)

| Source | d.f. | SS (Sum of Squares) | MS (Mean Square) | F |

|---|---|---|---|---|

| Regression | k | SSR=\sum_{i=1}^n(\hat y_i - \overline y)^2 | MSR = \frac{SSR}k | \frac{MSR}{MSE} |

| Residual (Error) | n-k-1 | SSE=\sum_{i=1}^n(y_i - \hat y_i)^2 | MSE = \frac{SSE}{n-k-1}=s^2 | |

| Total | n-1 | SST=\sum_{i=1}^n(y_i - \overline y)^2 |

- alternative ANOVA calculations:

- SST = \boldsymbol{y'y} - n\boldsymbol{\overline y}^2

- SSE = \boldsymbol{y'y} - \boldsymbol{\hat \beta'}X'X\boldsymbol{\hat\beta}

- SSR = SST - SSE = \boldsymbol{\hat \beta'}X'X\boldsymbol{\hat\beta} - n\boldsymbol{\overline y}^2

- multiple R^2:

"usefulness" of regression...

- R^2 = \frac{SSR}{SST} = 1 - \frac{SSE}{SST} (variation due to regression over total variation)

- adding a variable to a model increases the regression sum of squares, and hence R^2

- if adding a variable only marginally increases R^2, it might cast doubt on its inclusion in the model

- F-test: H_0:

\beta_1 = ... = \beta_k = 0 vs. H_A: at least one \beta_j \neq 0

- alternative: H_{restrict}: E(y) = \beta_0 vs. H_{full}: E(y) = \beta_0 + \beta_1 x_1 + ... + \beta_k x_k

- F = \frac{MSR}{MSE} \sim

F_{k, n-k-1}

(bottom of R output)

- quantile approach: reject H_0 if F > F_{k,n-k-1, 1-\alpha}

- probability approach: reject H_0 if P(F_{random} > F) < \alpha where F_{random} \sim F_{k,n-k-1}

- t-test: H_0:

\beta_j = 0 vs. H_A: \beta_j \neq 0

- t = \frac{\hat

\beta_j}{se(\hat\beta_j)} \sim t_{n-k-1}

- reject H_0 if 2\cdot P(T>|t|) < \alpha where T \sim t_{n-k-1}

- 100(1-\alpha)\% confidence interval for \beta_j: \hat \beta_j \pm t_{n-k-1, 1-\alpha/2}\cdot se(\hat\beta_j)

- t = \frac{\hat

\beta_j}{se(\hat\beta_j)} \sim t_{n-k-1}

- linear combination of coefficients: for when we want to estimate a result

with given predictors

- example (book): estimating avg. formaldehyde concentration in homes with

UFFI (x_1 = 1) and airtightness 5

(x_2 = 2)

- \theta = \beta_0 + \beta_1 + 5 \beta_2 = \boldsymbol{a'\beta} with \boldsymbol{a'} = (1,1,5)

- estimate: \hat \theta = \boldsymbol{a'\hat\beta} = (1,1,5)\begin{pmatrix}31.37\\9.31\\2.85\end{pmatrix} = 54.96

- example (book): estimating avg. formaldehyde concentration in homes with

UFFI (x_1 = 1) and airtightness 5

(x_2 = 2)

- additional sum of squares principle (linear hypthoseses): testing

simultaneous statements about several parameters

- example:

- full model: y = \beta_0 + \beta_1x_1 + \beta_2x_2 + \beta_3x_3 + \epsilon

- restrictions: each restriction is one equation equaling 0

- \beta_1 = 2\beta_2 (or \beta_1 - 2\beta_2 = 0)

- \beta_3 = 0

- matrix form: matrix A \in a \times

(k+1) has one row

for each restriction and one column per parameter (+ full rank)

- \begin{pmatrix}0 & 1 & -2 & 0 \\ 0 & 0 & 0 & 1\end{pmatrix} \begin{pmatrix}\beta_0 \\ \beta_1 \\ \beta_2 \\ \beta_3\end{pmatrix} = \begin{pmatrix}0\\0\end{pmatrix}

- hypothesis: H_0:

A\boldsymbol\beta = \boldsymbol 0

vs. H_A: at

least one of these \beta_j \neq 0

- alternative: H_{restrict}: \mu = \beta_0 + \beta_1x_1 + \beta_2x_2 + \beta_3x_3 vs. H_{full}: \mu = \beta_0 + \beta_1x_1 + \beta_2x_2 + \beta_3x_3 + \beta_4x_4 + \beta_5x_5 + \beta_6x_6

- restricted model: y = \beta_0 + \beta_2(2x_1 + x_2) + \epsilon

- additional sum of squares: SSE_{restrict} - SSE_{full}

- (!) for \mu = \beta_0: SSE_{restrict} = SST

- test statistic: F = \frac{(SSE_{restrict}-SSE_{full})/a}{SSE_{full} /

(n-k-1)} \sim F_{a,n-k-1}

for a rows in

A, k

parameters, n

observations

- reject H_0 if p-value < \alpha

- example:

Specification

- one-sample problem: y_i =

\beta_0 + \epsilon_i

- y_1, ... , y_n observations taken under uniform conditions from a stable model with mean level \beta_0

- E(y_i) = \beta_0

- E(\boldsymbol y) = X

\boldsymbol\beta

- \boldsymbol y = (y_1, ... y_n)'

- X = (1,...,1)'

- \boldsymbol \beta = \beta_0

- \hat\beta_0 = \overline y

- \hat\sigma^2 = s^2 = \frac{s_{yy}}{n-1} = \frac{\sum_{i=1}^n(y_i-\overline y)^2}{n-1}

- SSE = SST

- in R:

lm(y~1)

- two-sample problem: y_i =

\begin{cases}\beta_1 + \epsilon_i & i = 1,2,..,m \\ \beta_2+ \epsilon_1 & i = m + 1,

... , n\end{cases}

- y_1,...y_m taken under one set of conditions (standard process), mean \beta_1

- y_{m+1},...,y_n taken under another set of conditions (new process), mean \beta_2

- alternative: y_i = \beta_1x_{i1} + \beta_2x_{i2} +

\epsilon_i

- E(y_i) = \beta_1x_{i1} + \beta_2x_{i2}

- x_{i1}, x_{i2}

indicator variables

- x_{i1} = \begin{cases}1 & i = 1,2,...,m \\ 0 & i = m+1,...,n\end{cases}

- x_{i2} = \begin{cases}0 & i = 1,2,...,m \\ 1 & i = m+1,...,n\end{cases}

- E\begin{pmatrix}y_1 \\ \vdots \\ y_m \\ y_{m+1}

\\ \vdots \\ y_n \end{pmatrix} = \begin{pmatrix}1 \\ \vdots \\ 1 \\ 0 \\

\vdots \\ 0 \end{pmatrix} \beta_1 + \begin{pmatrix}0 \\ \vdots \\ 0 \\ 1 \\

\vdots \\ 1 \end{pmatrix} \beta_2

- matrix form E(\boldsymbol y) = X \boldsymbol

\beta

- X = \begin{pmatrix}1 & 0\\ \vdots & \vdots \\ 1 & 0\\ 0 & 1 \\ \vdots & \vdots \\ 0 & 1 \end{pmatrix}

- \boldsymbol \beta = \begin{pmatrix}\beta_1 \\ \beta_2 \end{pmatrix}

- matrix form E(\boldsymbol y) = X \boldsymbol

\beta

- in R:

lm(y~x1+x2-1) - hypothesis: \beta_1 = \beta_2

- polynomial models:

- linear: y_i = \beta_0 + \beta_1x_i + \epsilon_i

- X=\begin{pmatrix}1 & x_1 \\ \vdots & \vdots \\ 1 & x_n \end{pmatrix}

lm(y~x)

- quadratic: y_i = \beta_0 + \beta_1x_i + \beta_2x_i^2 +

\epsilon_i

- X=\begin{pmatrix}1 & x_1 & x_1^2 \\ \vdots & \vdots& \vdots \\ 1 & x_n & x_n^2\end{pmatrix}

lm(y~x+I(x^2))

- k-th

degree: y_i = \beta_0 + \beta_1 x_i + ... + \beta_kx_i^k +

\epsilon_i

- X=\begin{pmatrix}1 & ... & x_1^k \\ \vdots & \ddots & \vdots \\ 1 & ... & x_n^k \end{pmatrix}

lm(y~poly(x, degree=k, raw=T))

- linear: y_i = \beta_0 + \beta_1x_i + \epsilon_i

- systems of straight lines: yields of a chemical process which changes linearly with

temperature...

- y_1, ..., y_m: yields of a chemical process at temperatures t_1,...,t_m in the absence of a catalyst (x_i = 0)

- y_{m+1},...,y_{2m}: yields of a chemical process at the same temperatures t_1,...,t_m in the presence of a catalyst (x_i = 1)

- case a (main effects): the catalyst has an effect; the effect is the

same at all temperatures

- \mu_i = \begin{cases}\beta_0 + \beta_1 t_i & i = 1,2,...,m \\ \beta_0+\beta_1t_{i-m}+\beta_2&i=m+1,...,2m\end{cases}

- alternative (indicator variable): E(y_i) = \beta_0 +

\beta_1t_i + \beta_2x_i

- x_i = \begin{cases}0 & i = 1,2,...,m \\ 1 & i = m+1,...,2m\end{cases}

- t_{i+m} = t_i, i = 1,2,...,m

- matrix form: E(\boldsymbol y) =

X \boldsymbol \beta

- \boldsymbol y = \begin{pmatrix}y_1\\\vdots\\ y_m \\ y_{m+1} \\ \vdots \\ y_{2m}\end{pmatrix}

- X=\begin{pmatrix}1 & t_1 & 0 \\ \vdots & \vdots & \vdots \\ 1 & t_m & 0 \\ 1 & t_1 & 1 \\ \vdots & \vdots & \vdots \\ 1 & t_m & 1 \end{pmatrix}

- \boldsymbol \beta = \begin{pmatrix}\beta_0 \\ \beta_1 \\\beta_2\end{pmatrix}

- hypothesis: \beta_2 = 0

- case b (interaction): the catalyst has an effect; the effect

changes with temperature

- \mu_i = \beta_0 + \beta_1t_i + \beta_2x_i + \beta_3t_ix_i\;\;\;\;i = 1,2,...,2m

- catalyst absent (x_i = 0): \mu_i = \beta_0 + \beta_1t_i\;\;\;\;i=1,2,...,m

- catalyst present (x_i = 1):

\mu_i = \beta_0 +

\beta_1t_{i-m}+\beta_2+\beta_3t_{i-m}\;\;\;\;i = m+1,...,2m

- \mu_i = \beta_0 + \beta_2 + (\beta_1 + \beta_3)t_{i-m}

- matrix form: E(\boldsymbol y) =

X \boldsymbol \beta

- \boldsymbol y = \begin{pmatrix}y_1\\\vdots\\ y_m \\ y_{m+1} \\ \vdots \\ y_{2m}\end{pmatrix}

- X=\begin{pmatrix}1 & t_1 & 0 & 0 \\ \vdots & \vdots & \vdots& \vdots \\ 1 & t_m & 0 & 0 \\ 1 & t_1 & 1 & t_1 \\ \vdots & \vdots & \vdots& \vdots \\ 1 & t_m & 1 & t_m \end{pmatrix}

- \boldsymbol \beta = \begin{pmatrix}\beta_0 \\ \beta_1 \\\beta_2\\\beta_3\end{pmatrix}

- hypothesis: \beta_2 = \beta_3 =

0 (no rejection

\to catalyst has

no effect)

- catalyst depends on temperature? \beta_3 = 0

- one-way classification (k-sample problem): comparison of several

"treatments"; generalization of the two-sample problem

- k

catalysts, n_i

observations with the i-th catalyst

(i = 1,...,k)

- n = n_1 + ... + n_k total observations

- y_{ij}:

j-th

observation from the i-th catalyst

group (i=1,...,k;\;\;j=1,...,n_i)

- E(y_{ij}) = \beta_i

- matrix form: E(\boldsymbol y) = X \boldsymbol \beta = \beta_1

\boldsymbol x_1 + ... + \beta_k \boldsymbol x_k

- \boldsymbol x_i:

regressor vectors indicating the group membership of the observations

- x_{ji} = \begin{cases}1&y_{ij} \text{ from group } i\\0&\text{otherwise}\end{cases}

- example (3 groups):

- \boldsymbol y = \begin{pmatrix} y_{11} \\ \vdots \\ y_{1n_1} \\ y_{21} \\\vdots \\ y_{2n_2} \\ y_{31}\\\vdots \\\ y_{3n_3} \end{pmatrix}

- X = (\boldsymbol x_1, \boldsymbol x_2, \boldsymbol x_3) = \begin{pmatrix}1 & 0 & 0 \\ \vdots & \vdots & \vdots \\ 1 & 0 & 0 \\ 0 & 1 & 0 \\ \vdots & \vdots & \vdots \\ 0 & 1 & 0 \\ 0 & 0 & 1 \\ \vdots & \vdots & \vdots \\ 0 & 0 & 1\end{pmatrix}

- \boldsymbol \beta = \begin{pmatrix}\beta_1 \\ \beta_2 \\ \beta_3 \end{pmatrix}

- \boldsymbol x_i:

regressor vectors indicating the group membership of the observations

- LSE: \hat \beta_i = \overline y_i

- hypothesis: \beta_1 = \beta_2 = ... = \beta_k

- alternative (reference group): relate group means to the mean of a

reference group (here, the first group)

- \beta_i = \beta_1 + \delta_i,\;\;\; i = 2,3,...k

- E(y_{ij})=\begin{cases}\beta_1&i=1\\\beta_1+\delta_i&i=2,...,k\end{cases}

- matrix form: E(\boldsymbol y) =

X\boldsymbol \beta

where X = (\boldsymbol 1,\boldsymbol x_2, ...,

\boldsymbol x_k) and \boldsymbol \beta =

(\beta_1, \delta_2, ..., \delta_k)'

- example (3 groups):

- X = (\boldsymbol 1,\boldsymbol x_2, \boldsymbol x_3) = \begin{pmatrix}1 & 0 & 0 \\ \vdots & \vdots & \vdots \\ 1 & 0 & 0 \\ 1 & 1 & 0 \\ \vdots & \vdots & \vdots \\ 1 & 1 & 0 \\ 1 & 0 & 1 \\ \vdots & \vdots & \vdots \\ 1 & 0 & 1\end{pmatrix}

- \boldsymbol \beta = \begin{pmatrix}\beta_1 \\ \delta_2 \\ \delta_2 \end{pmatrix}

- LSE: \hat{\boldsymbol\beta} = (\overline y_1,\;\; \overline y_2 - \overline y_1,\;\; ...,\;\; \overline y_k - \overline y_1)'

- k

catalysts, n_i

observations with the i-th catalyst

(i = 1,...,k)

- multicollinearity: in the presence of one variable, the other is not important

enough to have it included; the two variables express the same information, so there is no point to

include both (p. 157 / 171)

- typically shown by the fact that, in a model which includes both covariates, neither is significant on its own (t-test)

- orthogonality: special properties for X matrices

with orthogonal columns (dot product of any two columns 0)...

- non-changing estimates: \beta_i remains the same, regardless of how many variables there are in the model

- additivity of SSRs: SSR(x_1, ... , x_k) = SSR(x_1) + ... + SSR(x_k), for a differing number of variables in a model

- orthogonal \implies independence: the components of \boldsymbol{\hat\beta} are independent (covariances between \beta_i zero)

Model Diagnostics

- possible reasons for a model being

inadequate:

- inadequate functional form: missing needed variables and nonlinear components

- incorrect error specification: non-constant Var(\epsilon_i), non-normal distribution, non-independent errors

- unusual observations: outliers playing a big part

- residual

analysis: using the residual to assess the adequacy of a model

- residual:

\boldsymbol e = \boldsymbol

y - \boldsymbol{\hat y}

- \boldsymbol{\hat y}=H\boldsymbol y

- i-th case in dataset: e_i = y_i - \hat y_i

- estimates the random component \boldsymbol \epsilon

- E(\boldsymbol e) = (I-H)E(\boldsymbol

y)

- correctly specified model: E(\boldsymbol e) = \boldsymbol

0

- E(\boldsymbol e) = (I-H)E(\boldsymbol y) = (I-H)X\boldsymbol \beta = ... = X\boldsymbol\beta - X\boldsymbol\beta = \boldsymbol 0

- incorrectly specified model: E(\boldsymbol e) \neq \boldsymbol

0

- "true" model: E(\boldsymbol y) = X

\boldsymbol \beta + \boldsymbol u \gamma

- \boldsymbol u: regressor vector not in L(X)

- \gamma: a parameter

- E(\boldsymbol e) = (I-H)E(\boldsymbol y) = (I-H)(X\boldsymbol\beta + \boldsymbol u \gamma) = \gamma(I-H)\boldsymbol u \neq 0

- "true" model: E(\boldsymbol y) = X

\boldsymbol \beta + \boldsymbol u \gamma

- correctly specified model: E(\boldsymbol e) = \boldsymbol

0

- \boldsymbol e

and \boldsymbol{\hat

y}

should be uncorrelated

- fitted values should not carry any information on the residuals

- in other words: a graph of the residuals against the fitted values should show no patterns

- properties: for \boldsymbol y = X \boldsymbol \beta + \boldsymbol

\epsilon,

where h_{ij}

are elements of H...

- Var(\epsilon_i) = \sigma^2

constant

- Var(e_i) = \sigma^2(1-h_{ii}) not constant

- Cov(\epsilon_i, \epsilon_j) = 0,\;\;\; i \neq

j

uncorrelated

- Cov(e_i, e_j) = -\sigma^2h_{ij},\;\;\; i \neq j not uncorrelated

- Var(\epsilon_i) = \sigma^2

constant

- standardized residuals: residuals standardized to have approx. mean zero

and variance one

- definition: e_i^s=\frac{e_i}s

- recall: \hat\sigma^2 = s^2 = \frac{\boldsymbol{e'e}}{n-k-1}

- definition: e_i^s=\frac{e_i}s

- studentized

residuals: the dimensionless ratio resulting from the division of a

residual by an estimate of its standard deviation

- |d_i| > 2 or 3 would make us question whether the model is adequate for that case i

- a histogram or a dot plot of the studentized residuals helps us assess whether one or more of the residuals are unusually large

- residual:

\boldsymbol e = \boldsymbol

y - \boldsymbol{\hat y}

- serial correlation

(autocorrelation): if a regression model is fit to time series data

(e.g. monthly, yearly...), it is likely that errors are serially correlated (as opposed to the

errors \epsilon_t

being independent for time indices t)

- positively autocorrelated: a positive error last time unit implies a similar positive error this time unit

- detection: calculate lag k

sample autocorrelation r_k

of the residuals (r_0 = 1)

- measures the association within the same series (residuals) k steps apart

- sample correlation between e_t and its k-th lag, e_{t-k}

- lag k autocorrelation always between -1 and +1

- graphically: plot e_t against e_{t-k} and look for associations (positive: upwards, negative: downwards)

- in R:

acf(fit$residuals,las=1)

- autocorrelation function (of the residuals): graph of autocorrelations

r_k

as a function of the lag k

- two horizontal bands at \pm\frac2{\sqrt n}

are added to the graph

- sample autocorrelations that are outside these limits are indications of autocorrelation

- if (almost) all autocorrelations are within these limits, one can make the assumption of independent errors

- two horizontal bands at \pm\frac2{\sqrt n}

are added to the graph

- Durbin-Watson test: examines lag 1 autocorrelation r_1

in more detail; complicated to compute

- DW \approx 2: independent errors

- DW > 2 or DW < 2: correlated errors

- outlier: an observation that differs from the majority of the cases in the data set

- one must distinguish among outliers in the y (response) dimension (a) vs. outliers in the x (covariate) dimension (b) vs. outliers in both dimensions (c)

- x dimension: outliers that have unusual values on one or more of the covariates

- y

dimension: outliers are linked to the regression model

- random component too large?

- response or covariates recorded incorrectly?

- missing covariate?

- detection: graphically, studentized residual, leverage

- influence: an individual case has a major influence on a statistical procedure if the effects of the analysis are significantly altered when the case is omitted

- leverage: a measure

of how far away the independent variable values of an observation are from those of the other

observations

- definition: h_{ii} for i-th independent observation, i=1,..,n (entry in hat matrix H)

- properties:

- h_{ii} is a function of the covariates (x) but not the response

- h_{ii} is higher for x farther away from the centroid \overline x

- \sum_{i=1}^n h_{ii} = tr(H)= k+1

- \overline h =\frac{k+1}n

- rule of thumb: a case for which the leverage exceeds twice

the average is considered a high-leverage case

- formally: h_{ii} > 2\overline h = \frac{2(k+1)}n

- influence: study how the deletion of a case affects the parameter estimates

- after deleting the i-th case: \boldsymbol y = X \boldsymbol \beta + \boldsymbol \epsilon for the remaining n-1 cases

- \boldsymbol{\hat\beta}_{(i)}: the estimate of \boldsymbol\beta without the i-th case

- \boldsymbol{\hat\beta}: the estimate of \boldsymbol\beta for all cases

- influence of the i-th case: \boldsymbol{\hat\beta} - \boldsymbol{\hat\beta}_{(i)}

- Cook's D

statistic: estimate of the influence of a data point when performing a

least-squares regression analysis

- D_i > 0.5 should be examined

- D_i > 1 great concern

Lack of Fit

- lack of fit test: can be performed if there are repeated observations at some of

the constellations of the explanatory variables

- formally: for n

observations, only k

different values of x were

observed

- there were n_i values of y measured at covariate value x_i,\;\; i = 1,...,k

- x_1: y_{11},...,y_{1n_1}\\\vdots\\x_k: y_{k1},...,y_{kn_k}

- one-way classification model: y_{ij} = \beta_1I(x_i = x_1) + ... + \beta_kI(x_i =

x_k) + \epsilon_{ij}

- so, in essence, each individual result for a certain constellation x_i is just \beta_i + \epsilon_{ij}

- E(\epsilon_{ij})=0

- Var(\epsilon_{ij}) = \sigma^2

- matrix form: \boldsymbol y = X \boldsymbol{\beta +

\epsilon}

- \boldsymbol y \in n \times 1: vector of responses, n = \sum_{i=1}^kn_i

- X \in n \times k: design matrix with ones and zeros representing the k groups

- \boldsymbol \beta \in k \times 1: vector of unknown means \mu_i

- (\hat\beta_1, ...,

\hat\beta_k) = (\overline y_1, ..., \overline y_k)

- \overline y_i = \frac1{n_i}\sum_{j=1}^{n_i}y_{ij} (avg. of group i)

- restricted (parametric) model: y_{ij} = \beta_0 + \beta_1x_i + \epsilon_{ij} estimate via least squares

- PESS: PESS= SSE_{full} =

\sum_{i=1}^k\sum_{j=1}^{n_i}(y_{ij}-\overline y_i)^2

- d.f. number of observations minus number of groups (n-k)

- LFSS: LFSS = \sum_{i=1}^k n_i(\overline y_i - \hat \beta_0 -

\hat \beta_1 x_i)^2 \geq 0

- d.f. number of groups k - number of parameters (lin: 2 params.)

- SSE_{restrict} = PESS + LFSS

- SSE_{restrict} \geq SSE_{full}

- test (linear): H_{restrict}: \mu_{i} = \beta_0 +

\beta_1x_i

vs. H_{full} = \mu_i =

\beta_1I(x_i=x_1) + ... + \beta_kI(x_i=x_k)

- F=\frac{LFSS/(k-2)}{PESS/(n-k)} \sim F_{k-2,n-k}

- reject H_0 \implies lack of fit, reject restricted model

- test (general): H_{restrict}: \mu_i = \beta_0 + \beta_1x_i +

\beta_2x_i^2 + ... vs. H_{full} = \mu_i =

\beta_1I(x_i=x_1) + ... + \beta_kI(x_i=x_k)

- F=\frac{LFSS/(k-\dim(\beta))}{PESS/(n-k)} \sim F_{k-\dim(\beta),n-k}

- formally: for n

observations, only k

different values of x were

observed

- variance-stabilizing

transformations: find a simple function g to apply to

values x in a data set to

create new values y =

g(x) such that the variability of

the values y is not

related to their mean value

- assume y = \mu + \epsilon where \mu is a

fixed mean

- Var(y) = (h(\mu))^2\sigma^2 has a non-constant variance that depends on the mean

- h known

- goal: find g(x) such that Var(g(x)) is constant and does not depend on \mu

- Var(g(y)) =

(g'(\mu))^2(h(\mu))^2\sigma^2

- goal: find g such that g'(\mu) = \frac1{h(\mu)}, such that finally Var(g(y)) \approx \sigma^2

- example: h(\mu) = \mu \implies g'(\mu) = \frac1\mu \implies g(\mu) = \ln(\mu)

- Box-Cox transformations: find \lambda s.t. the

transformed response y_i^{(\lambda)}

minimizes SSE(\lambda) (done in a table,

compare various \lambdas to their

SSE(\lambda)s)

- \lambda = 0: log transform

using limit

lm(log(...)~., data=...) - \lambda = \frac12:

square root transform

lm(sqrt(...)~., data=...) - \lambda = 1: no transform

lm(...~., data=...) - \lambda = 2: square

transform

lm((...)*(...)~., data=...) - in R:

library(MASS); boxcox(fit)

- \lambda = 0: log transform

using limit

- assume y = \mu + \epsilon where \mu is a

fixed mean

Model Selection

- goal: given observational data, find the best model which

incorporates the concepts of model fit and model simplicity

- increasing the number of predictors increases variability

in the predictions

- Var(\hat{\boldsymbol y}) = \sigma^2H \implies average variance \frac1n\sum_{i=1}^nVar(\hat{\boldsymbol y})=\frac{\sigma^2(k+1)}n for k covariates and sample size n

- multicollinearity: different methods of analysis may end up with final models that look very different, but describe the data equally well

- increasing the number of predictors increases variability

in the predictions

- model selection: given

observations on a repsonse y and q potential

explanatory variables v_1,...,v_q,

select a model y =

\beta_0 + \beta_1x_1 + ... + \beta_px_p + \epsilon where...

- x_1,...,x_p is a subset of the original regressors v_1,...,v_q

- no important variable is left out of the model

- no unimportant variable is included in the model

- all possible regressions: fit 2^q

models if q variables

are involved

- R_k^2 = 1 -

\frac{SSE_k}{SST}

for k

variables and k+1 regression

coefficients

- increase in k

means decrease in SSE_k,

approaching 0 when k=n-1

- increase in R^2 means decrease in s^2

- SST does not depend on the covariates; just on y (see definition)

- therefore, R^2 approaches 1 as k increases, so we don't use R^2, since we'd just choose the model with the most variables

- increase in k

means decrease in SSE_k,

approaching 0 when k=n-1

- R_{adj}^2:

adjusted R^2

- remedies the problem of R^2 continually increasing by dividing the degrees of freedom

- ideal model and choice of k:

highest R_{adj}^2

- equivalent: smallest s^2

- AIC: Akaike's Information

Criterion

- prefer models with smaller AIC

- BIC: Bayesian Information

Criterion

- larger penalty for more variables

- R_k^2 = 1 -

\frac{SSE_k}{SST}

for k

variables and k+1 regression

coefficients

- automatic model selection methods: forward selection, backward elimination,

stepwise regression (needed in R:

library(MASS))- forward selection: start with the smallest model, build up to the optimal

model

- in R:

stepAIC(lm(y~1, data=dataset), direction = "forward", scope = list(upper = lm(y~., data=dataset))[, k = log(nrow(dataset))])(for BIC:[...])

- in R:

- backward elimination: start with the largest model and build down to the

optimal model

- in R:

stepAIC(lm(y~., data=dataset), direction = "backward"[, k = log(nrow(dataset))])

- in R:

- stepwise regression: oscillate between forward selection and backward

elimination

- in R: use either previous function, but with

direction = "both"

- in R: use either previous function, but with

- forward selection: start with the smallest model, build up to the optimal

model

forward selection

INIT

M = intercept-only model

P = all covariates

REPEAT

IF P empty STOP

ELSE

calculate AIC for sizeof(P) models, each model containing one covariate in P is added to M

IF all AICs > AIC(M) STOP

ELSE

update M with covariate whose addition had minimum AIC

remove covariate from P

forward selection

INIT

M = intercept-only model

P = all covariates

REPEAT

IF P empty STOP

ELSE

calculate AIC for sizeof(P) models, each model containing one covariate in P is added to M

IF all AICs > AIC(M) STOP

ELSE

update M with covariate whose addition had minimum AIC

remove covariate from Pbackward elimination

INIT

M = model with all covariates

P = all covariates

REPEAT

IF P empty STOP

ELSE

calculate AIC for sizeof(P) models, each model without each of the covariates in P

IF all AICs > AIC(M) STOP

ELSE

update M by deleting covariate that led to minimum AIC

remove covariate from P

backward elimination

INIT

M = model with all covariates

P = all covariates

REPEAT

IF P empty STOP

ELSE

calculate AIC for sizeof(P) models, each model without each of the covariates in P

IF all AICs > AIC(M) STOP

ELSE

update M by deleting covariate that led to minimum AIC

remove covariate from Pstepwise regression INIT M = intercept-only model OR full model e = small threshold REPEAT UNTIL STOP do a forward step on M do a backward step on M # For both steps, the differences in AIC need to be # greater than e for the selection to go forward, otherwise # the changes can keep undoing each other.

stepwise regression

INIT

M = intercept-only model OR full model

e = small threshold

REPEAT UNTIL STOP

do a forward step on M

do a backward step on M

# For both steps, the differences in AIC need to be

# greater than e for the selection to go forward, otherwise

# the changes can keep undoing each other.Nonlinear Regression

- linear model (recap): y=\mu+\epsilon where \mu = \beta_0 + \beta_1x_1 + ... +

\beta_kx_k

- key: linearity of the parameters \beta_i

- the regressor variables x_i can be any known nonlinear function of the regressors...

- intrinsically nonlinear model: a nonlinear model that cannot be transformed into a

linear model

- counterexample: y = \alpha x_1^\beta x_2^\gamma\epsilon can be transformed into \ln(y)=\ln(\alpha)+\beta\ln(x_1)+\gamma\ln(x_2)+\ln(\epsilon)

- require iterative algorithms and convergence (vs. linear models, which are analytic)

- linear trend model: \mu_t

= \alpha + \gamma t

- \gamma: growth rate, unbounded

- \alpha: starting value at t=0

- nonlinear regression model: y_i = \mu_i + \epsilon_i = \mu(\boldsymbol x_i,

\boldsymbol\beta) + \epsilon_i

- \epsilon_i \sim N(0,\sigma^2) iid. for i=1,...,n

- \boldsymbol x_i = (x_{i1},...,x_{im})': vector of m covariates for the i-th case (typically m=1, where the covariate is time)

- \boldsymbol \beta: vector of p parameters to be estimated along with \sigma^2 (usually a different num. of parameters than covariates)

- \mu(\boldsymbol x_i, \boldsymbol\beta): nonlinear model component

- S(\boldsymbol{\hat\beta}) = \sum_{i=1}^n(y_i-\mu(\boldsymbol x_i, \boldsymbol \beta))^2

- estimates:

- \boldsymbol{\hat\beta}:

no closed form!

- use iterative function to minimize S(\boldsymbol{\hat\beta})

- \hat\sigma^2 = s^2 = \frac{S(\boldsymbol{\hat\beta})}{n-p} = \frac{\sum_{i=1}^n(y_i-\mu(\boldsymbol x_i, \boldsymbol \beta))^2}{n-p}

- \boldsymbol{\hat\beta}:

no closed form!

- Var(\boldsymbol{\hat\beta})

\approx s^2(X'X)^{-1}

- s.e.(\hat\beta_i) = \sqrt{v_{ii}} (the square roots of the diagonal elements in the covariance matrix provide estimates of the standard errors)

- off-diagonal elements provide estimates of the covariances among the estimates

- 100(1-\alpha)\% C.I. for \beta_j: \hat\beta_j \pm t_{n-p,1-\alpha/2}s.e.(\hat\beta_j)

- H_0: \beta_j =

0 vs. H_a: \beta_j \neq

0: t =

\frac{\hat\beta_j}{s.e.(\hat\beta_j)} \sim t_{n-p}

- for constants: H_0: \beta_j = c vs. H_a: \beta_j \neq c: t = \frac{\hat\beta_j - c}{s.e.(\hat\beta_j)} \sim t_{n-p}

- restricted models or goodness-of-fit tests can be performed similarly as for linear models

- in R:

fitnls = nls(y~(formula using a, b),start=list(a=...,b=...))

- Newton-Raphson method: a

root-finding algorithm which produces successively better approximations to the zeroes of a

real-valued function

- goal: find \boldsymbol\beta

that minimizes f(\boldsymbol \beta), here S(\boldsymbol

\beta) or -\log

L(\boldsymbol\beta)

- Df(\boldsymbol \beta) = (\frac{\partial f}{\partial \beta_1}, ... , \frac{\partial f}{\partial \beta_p})': the p-vector containing the first derivatives of f w.r.t. \beta_i

- D^2f(\boldsymbol \beta): the p \times p matrix of second derivatives with the ij-th element \frac{\partial^2 f}{\partial \beta_i \partial \beta_f} (Hessian matrix)

- general: initialize \boldsymbol\beta_{old} = starting value, then

repeat until convergence:

- \boldsymbol \beta_{new} \approx \boldsymbol \beta_{old} - (D^2f(\boldsymbol\beta_{old}))^{-1}Df(\boldsymbol\beta_{old})

- \boldsymbol \beta_{old} = \boldsymbol \beta_{new}

- problem: unstable due to inversion

- scoring: initialize \boldsymbol\beta_{old} = starting value, then

repeat until convergence:

- \boldsymbol \beta_{new} \approx \boldsymbol \beta_{old} + (I(\boldsymbol\beta_{old}))^{-1}D\log L(\boldsymbol\beta_{old})

- \boldsymbol \beta_{old} = \boldsymbol \beta_{new}

- information matrix: I(\boldsymbol\beta) = E(-D^2\log L(\boldsymbol \beta))

- problematic: local minima that "trap" iterative algorithms, parameters of highly varying magnitudes (e.g. one parameter in range 0-1, another in the thousands), badly specified models with non-identifiable parameters (similar to multicollinearity)

- goal: find \boldsymbol\beta

that minimizes f(\boldsymbol \beta), here S(\boldsymbol

\beta) or -\log

L(\boldsymbol\beta)

Time Series Models

- first-order autoregressive model (AR1): y_t = \mu(X_t, \beta) + \epsilon_t

- autocorrelations of observations 1 step apart: \phi

- all correlations among observations one step apart \phi are the same

- \phi = Corr(\epsilon_1, \epsilon_2) = ... =

Corr(\epsilon_{n-1}, \epsilon_n)

- |\phi| < 1 (correlations between -1 and +1)

- autocorrelations of observations k

steps apart: \phi^k

- \phi^k = Corr(\epsilon_1, \epsilon_{k+1}) = ... = Corr(\epsilon_{n-k}, \epsilon_n)

- properties of autocorrelations:

- they depend only on the time lag between the observations (so the time indices don't matter; just the time distance)

- they decrease exponentially with the time lag (because -1 < \phi <

1)

- the farther apart the observations, the weaker the autocorrelation

- if \phi is close to 1, the decay is slow

- autocorrelation functions (lag k

correlation): \rho_k = \phi^k = Corr(\epsilon_{t-k},

\epsilon_t)

- \rho_0 = 1

- \rho_k = \rho_{-k}

- correlated error at time t: \epsilon_t =

\phi\epsilon_{t-1} + a_t

where a_t \sim N(0,

\sigma_a^2)

- white noise (random shocks): a_t

- a_t

is the "usual" regression model error; mean 0, all uncorrelated

- Corr(a_{t-k},a_t) = 0 for all k \neq 0

- a_t

is the "usual" regression model error; mean 0, all uncorrelated

- expanded: \epsilon_t = a_t + \phi a_{t-1} + \phi^2a_{t-2} + ...

- E(\epsilon_t) = 0

- Var(\epsilon_t) \to \frac{\sigma_a^2}{1-\phi^2}

- white noise (random shocks): a_t

- stationary model: fixed level 0; realizations scatter around the fixed level and sample paths don't leave this level for long periods

- in R:

library(nlme); fitgls=gls(y~x,correlation=corARMA(p=1,q=0))(changep=2for AR2)

- autocorrelations of observations 1 step apart: \phi

- random walk model: y_t =

\mu(X_t, \beta) + \epsilon_t

- \phi = 1

- \epsilon_t = \epsilon_{t-1}

+ a_t = a_t + a_{t-1} + a_{t-2} + ...

- cumulative sum of all random shocks up to time t

- nonstationary model: no fixed level; paths can deviate for long periods from the starting point

- first-order difference: w_t = \epsilon_t - \epsilon_{t-1} = a_t

- well-behaved, stationary, uncorrelated

- effects of ignoring autocorrelation: what happens when we fit a standard linear

model even if the errors are correlated?

- stationary errors: variance of \hat\beta

will be overestimated compared to the true variance

(inefficiency)

- t ratios too small \to null hypothesis less likely to be rejected when it should be

- non-stationary errors: variance of \hat\beta

will be underestimated compared to the true variance

- t ratios too large \to null hypothesis likely to be rejected when it shouldn't be

- stationary errors: variance of \hat\beta

will be overestimated compared to the true variance

(inefficiency)

- forecasting (prediciton): given data up to time period n, predict response

at time period n +

r (r step-ahead

forecast)

- r

step-ahead forecast: y_n(r) = \hat y_{n+r}

- n: forecast origin

- r: forecast horizon

- assumption: future values of the covariate x_t are known (e.g. own future investments)

- 1 step forecast (AR1, one covariate): assume x_{n+1}

known...

- observation: y_{n+1} = \phi y_n + (1-\phi)\beta_0 + (x_{n+1}-\phi x_n)\beta_1 + a_{n+1}

- prediction: \hat y_{n+1} = \hat

\phi y_n + (1-\hat\phi)\hat\beta_0 + (x_{n+1}-\hat\phi

x_n)\hat\beta_1

- 95% CI: \hat y_{n+1} \pm 1.96se(\hat y_{n+1})

- general step forecast (AR1, one covariate): \hat y_{n+r} = \hat \phi

\hat y_{n+r-1} + (1-\hat\phi)\hat\beta_0 + (x_{n+r}-\hat\phi

x_{n+r-1})\hat\beta_1

for r \geq 2

- 95% CI: \hat y_{n+r} \pm 1.96se(\hat y_{n+r})

- r

step-ahead forecast: y_n(r) = \hat y_{n+r}

Logistic Regression

- logistic regression:

regression where the response variable is binary (general:

categorical)

- y_i:

outcome of case i, \;\;\; i = 1,2,...,n

- y_i\sim Ber(\pi), independent

- P(y_i=1)=\pi

(success)

- \ln\left(\frac{\pi(x_i)}{1-\pi(x_i)}\right)=x'_i\beta

= \beta_0 + \beta_1x_{i1}+...+\beta_px_{ip}

- \pi(x_i)=\frac{e^{x_i'\beta}}{1+e^{x_i'\beta}}

- 1-\pi(x_i)=\frac{1}{1+e^{x_i'\beta}}

- \beta_0: inflection point

- \beta_1: steepness of sigmoid-like function

- risk of y for factor x: \pi(x) = P(y=1|x)=\frac{e^{x'\beta}}{1+e^{x'\beta}}

- odds of y

for a fixed x:

Odds(x) =

\frac{\pi(x)}{1-\pi(x)}=\frac{P(y=1|x)}{1-P(y=1|x)}=\exp(x'\beta)

- how much higher is the probability of the occurrence y compared to the nonoccurrence of y?

- odds of n:1 \implies occurence is n times more likely than nonoccurence

- odds ratio: OR=\frac{Odds(x=1)}{Odds(x=0)}=\frac{\frac{P(y=1|x=1)}{P(y=0|x=1)}}{\frac{P(y=1|x=0)}{P(y=0|x=0)}}

- \beta=\ln\left(\frac{\pi(x+1)}{1-\pi(x+1)}\right)-\ln\left(\frac{\pi(x)}{1-\pi(x)}\right)=\ln(OR)

vector of log odds ratios

- \exp(\beta)=OR

- what is the multiplicative factor by which the odds

of occurrence increase / decrease for a change from

x

to x+1?

- e.g. \beta = -0.2 \to \exp(\beta) = 0.82 \implies a change from x to x+1 decreases the odds of occurence by 18\%

- for k units: \beta k with ratio measured as \exp(\beta k)

- \beta=\ln\left(\frac{\pi(x+1)}{1-\pi(x+1)}\right)-\ln\left(\frac{\pi(x)}{1-\pi(x)}\right)=\ln(OR)

vector of log odds ratios

- \ln\left(\frac{\pi(x_i)}{1-\pi(x_i)}\right)=x'_i\beta

= \beta_0 + \beta_1x_{i1}+...+\beta_px_{ip}

- P(y_i=0)=1-\pi (failure)

- E(y_i)=\pi

- P(y_i=1)=\pi

(success)

- y_i\sim Ber(\pi), independent

- one covariate model: \exp(x'\beta) = \beta_0 + \beta_1 x

- \ln\left(\frac{P(y=1|x)}{1-P(y=1|x)}\right)=\beta_0+\beta_1x

- Odds(x)=\frac{P(y=1|x)}{1-P(y=1|x)}=\exp(\beta_0+\beta_1x)

- Odds(x=0)=\exp(\beta_0+\beta_1 \cdot 0) = \exp(\beta_0)

- Odds(x=1)=\exp(\beta_0+\beta_1 \cdot 1) = \exp(\beta_0 + \beta_1)

- OR = \frac{Odds(x=1)}{Odds(x=0)}=\exp(\beta_1)

- \beta_1 = \ln(OR)

- H_0: \beta_1 = 0 (no assoc. between x and y)

- \beta_0 = \ln(Odds(x = 0))

- MLE \hat \beta: Newton-Raphson...

- CIs and tests:

- 100(1-\alpha)\% CI for \ln(OR): \hat\beta_j \pm z_{1-\alpha/2}se(\hat\beta_j)

- 100(1-\alpha)\% CI for OR: \exp(\hat\beta_j \pm z_{1-\alpha/2}se(\hat\beta_j))

- Wald test: H_0: \beta_j = 0 vs. H_A: \beta_j \neq 0: \frac{\hat\beta_j}{se(\hat\beta_j)}\sim N(0,1)

- case: an individual observation

- constellation: grouped information at distinct levels of the explanatory

variables

- n_k; number of cases at the k-th constellation

- y_k: number of successes at the k-th constellation

- prob. of success for k-th constellation: \pi(x_k, \beta) = \frac{\exp(x_k\beta)}{1+\exp(x_k\beta)}

- likelihood ratio tests (LRT): used to compare the maximum likelihood under

the current model (the “full” model), with the maximum likelihood obtained under alternative

competing models ("restricted" models)

- H_{restrict}: linear

predictor x'_{res}\beta_{res}

vs. H_{full}: linear

predictor x'\beta

- x_{res} subset of x

- LRT statistic: 2 \cdot

\ln\left(\frac{L(full)}{L(restrict)}\right) = 2 \cdot

\ln\left(\frac{L(\hat\beta)}{L(\hat\beta_{res})}\right) \sim

\chi_a^2

- equiv.: 2 \cdot (\ln(L(full))-\ln(L(restrict)))

- a = \dim(\beta) - \dim(\beta_{res})

- reject H_{restrict} if statistic greater than corresponding chi-square value

- large value \implies the success probability depends on one or more of the regressors (i.e. full model better)

- small value \implies none of the regressors in the model influence the success probability

- H_{restrict}: linear

predictor x'_{res}\beta_{res}

vs. H_{full}: linear

predictor x'\beta

- deviance: twice the log-likelihood ratio between the saturated model and

the parameterized (full) model; m

constellations

- saturated model: each constellation of the explanatory variables is

allowed its own distinct success probability

- \hat\pi_k = \frac{y_k}{n_k}

- D = 2\frac{\ln(L(saturated))}{\ln(L(full))} = 2

\cdot \ln \left(\frac{L(\hat\pi_1,...,\hat\pi_m)}{L(\hat\beta)}\right) \sim

\chi_a^2

- a = m - \dim(\beta)

- LRT = D(restricted) - D(full)

- p-value:

1 - pchisq(D, 𝑎)

- saturated model: each constellation of the explanatory variables is

allowed its own distinct success probability

- y_i:

outcome of case i, \;\;\; i = 1,2,...,n

- in R:

freqs <- cbind(yes, no); fit <- glm(freqs~x[+...], family="binomial")

Poisson Regression

- generalized linear model

(GLM): generalizes linear regression by allowing the linear model to be related

to the response variable via a link function

- response variables y_1,...y,_n: share the same distribution from the exponential family (Normal, Poisson, Binomial...)

- parameters \beta and explanatory variables x_1,...x_p

- monotone link function g:

relates a transform of the mean \mu_i

linearly to the explanatory variables

- g(\mu_i) = \beta_0 + \beta_1x_{i1} + ... + \beta_px_{ip}

- standard linear regression: g(\mu) = \mu (identity function)

- logistic regression: g(\mu) = \ln\left(\frac\mu{1-\mu}\right) (logit)

- Poisson regression: g(\mu) = \ln(\mu)

- Poisson regression model: response represents count data (e.g.

number of daily equipment failures, weekly traffic fatalities...)

- P(Y = y) = \frac{\mu^y}{y!}e^{-\mu},\;\;\;y=0,1,2,...

- E(y) = Var(y) = \mu > 0

- g(\mu)=\ln(\mu)=

\beta_0+\beta_1x_1+...+\beta_px_p

- \mu=\exp(\beta_0+\beta_1x_1+...+\beta_px_p)

- interpretation of coefficients: changing x_i

by one unit to x_i+1 while keeping all

other regressors fixed affects the mean of the response by 100(\exp(\beta_i)-1)\%

- example: \frac{\exp(\beta_0+\beta_1(x_1+1)+...+\beta_px_p)}{\exp(\beta_0+\beta_1x_1+...+\beta_px_p)}=\exp(\beta_1)

- 95% CI: \hat\beta \pm 1.96se(\hat\beta)

- for the mean ratio \exp(\beta): \exp(\hat\beta \pm 1.96se(\hat\beta))

- everything else identical to logistic regression

Linear Mixed Effects Models

- linear mixed effects models: some subset of regression parameters vary randomly

from one individual to another

- individuals are assumed to have their own subject-specific mean response trajectories over time

- simple mixed effects model: Y_{ij} = \beta + b_i + e_{ij}

(observation = population mean + individual deviation + measurement error)

- \beta: population mean (fixed effects, constant)

- b_i:

individual deviation from the population mean (random

effects) (i-th

individual)

- b_i \sim N(0,d)

- positive: individual responds higher than population average (higher on y-axis)

- negative: individual responds lower than population average (lower on y-axis)

- e_{ij}:

within-individual deviations (measurement error) (i-th

individual, j-th

observation)

- e_{ij} \sim N(0,\sigma^2)

- E(Y_{ij}) = \beta

- Var(Y_{ij}) = d + \sigma^2

- Cov(Y_{ij},Y_{km}) = 0 for i \neq k

- Cov(Y_{ij},Y_{ij}) = Var(Y_{ij}) = d + \sigma^2

- Cov(Y_{ij},Y_{ik}) = d

- Cor(Y_{ij},Y_{km}) = 0 for i \neq k

- Cor(Y_{ij},Y_{ij}) = 1

- Cor(Y_{ij},Y_{ik}) = \frac{d}{d+\sigma^2}

- in R: matrix format, n

rows for n

individuals and m

columns for m

time points per individual

- has to be transformed into longitudinal format for use with

lme

- has to be transformed into longitudinal format for use with

- general linear mixed effects model: Y_i = X_i\beta + Z_ib_i + e_i,\;\;b_i\sim

N_q(0,D),\;\;e_i\sim N_{n_i}(0,R_i), where R_i =

\sigma^2I_{n_i}

- Y_i \in \R^{n_i}: outcomes (for i-th individual, as for nearly everything here...)

- X_i \in \R^{n_i \times p}: design matrix for fixed effects

- Z_i \in \R^{n_i \times q}: design matrix for random effects (columns are usually subset of columns of X_i)

- \beta \in \R^p:

fixed effects

- any component of \beta can be allowed to vary randomly by including the corresponding column of X_i in Z_i

- b_i \in \R^q:

random effects

- independent of covariates X_i

- e_i \in \R^{n_i}: within-individual errors

- conditional mean: E(Y_i \;|\; b_i) = X_i\beta + Z_ib_i

- marginal mean: E(Y_i) = X_i\beta

- conditional variance: Var(Y_i\;|\;b_i) = R_i

- marginal variance: Var(Y_i) = Z_iDZ_i'+R_i

- \sigma^2_{REML}=\frac1{n-1}\sum_{i=1}^n(x_i-\overline x)^2 (unbiased, restricted maximum likelihood)

- \sigma^2_{ML}=\frac1{n}\sum_{i=1}^n(x_i-\overline x)^2 (biased)

- \hat b_i:

best linear unbiased predictor (BLUP)

- "shrinks" the i-th individual's predicted response profile towards the population-averaged mean response profile

- large R_i compared to D \implies more shrinkage to mean

- small R_i compared to D \implies closer to observed value

- large n_i \implies less shrinkage

Statistical Learning (Machine Learning)

- supervised learning: an outcome (which guides the learning process) predicted based

on a set of features

- unsupervised learning: no outcome; only features observed (not relevant here)

- outcome (outputs, responses, dependent variables): the thing to predict;

can be quantitative (ordered, e.g. stock price) or qualitative (unordered

here, categorical, factors, e.g species of Iris)

- predicting quantitative outcomes \to regression

- predicting qualitative outcomes \to classification

- features (inputs, predictors, independent variables): the data to make predcitions for the outcome

- training set: data set containing both features and outcomes to build the model

Prediction Methods

- least squares model (linear model): high stability but low

accuracy (high bias, low variance)

- goal: predict Y by

f(X) = X'\beta

- \beta_0: intercept (bias)

- X \in \R^p: random input vector (first element 1 for intercept)

- Y \in \R: random outcome (to predict)

- p(X,Y): joint distribution

- f(X): function

for predicting Y

based on X

- f'(X)=\beta \in \R^p: vector that points in the steepest uphill direction

- (x_1,y_1),...,(x_n,y_n): training data

- method: pick \beta to

minimize residual sum of squares RSS(\beta) = \sum_{i=1}^n(y_i -

x_i'\beta)^2

- matrix notation: RSS(\beta) = (y-X\beta)'(y-X\beta)

- LSE: \hat\beta = (X'X)^{-1}X'y

- fitted value: \hat y_i = x_i'\hat\beta

- theoretical: \beta = (E(X'X))^{-1}E(X'Y)

- should only be used when Y is continuous and Normal distributed

- goal: predict Y by

f(X) = X'\beta

- k-nearest

neighbor model: low stability but high accuracy (low bias,

high variance)

- use observations in training set closest in input space to x to form

\hat Y

- formally: f(x)=\frac1k\sum_{x_i \in

N_k(x)}y_i

- N_k(x): neighborhood of x defined by the k closest points x_i in the training sample

- find k observations with x_i closest to new x in input space, and average their responses

- formally: f(x)=\frac1k\sum_{x_i \in

N_k(x)}y_i

- use observations in training set closest in input space to x to form

\hat Y

Statistical Decision Theory

- loss function L(Y,f(X)): penalizes errors in

prediction

- expected prediction error: EPE(f) = E_{x,y}(L(Y,f(X)))

- expected (squared) prediction error: criterion for choosing f based on

the squared error loss function (L2)

- L2 Loss: L_2 = L(Y,f(X)) = (Y-f(X))^2 (most popular)

- EPE(f) = E_{x,y}(Y-f(X))^2 = \int\int(y-f(x))^2p(x,y)dxdy = \int(\int(Y-f(x))^2p(y|x)dy)p(x)dx = E_x(E_{y|x}((Y-f(X))^2|X))

- optimal Bayes classifier: minimize E_{y|x}((Y-f(X))^2\;|\;X) for all X

- f_{bayes}(X)=E_{y|x}(Y|X)

- nearest neighbor: f(x) =

Ave(y_i \; | \; x_i \in N_k(x))

- as n,k \to \infty, \frac kn\to 0: f(x) \to E(Y\;|\;X=x)

- L1 Loss: E|Y-f(X)|

(abs. value)

- f(x) = \text{median}(Y\;|\;X=x)

Categorical Data

- estimate \hat G: contains values in the set of possible classes \mathcal G where |\mathcal G| = K

- loss function: L \in

\R^{K \times K}

- zero on he diagonal

- nonnegative elsewhere

- L(k,l): price paid for classifying an observation belonging to class \mathcal G_k as \mathcal G_l

- zero-one loss function: all misclassifications are charged one unit

- L(k,l)=\begin{cases}0&k=l\\1&k \neq l\end{cases}

- EPE = E(L(G,\hat

G(X)))=E_x(E_{g|x}(L(G,\hat G(X))\;|\;X))

- E_{g|x}(L(G,\hat G(X))\;|\;X) =

\sum_{k=1}^KL(\mathcal G_k, f(X))p(\mathcal G_k \;|\; X)

- \sum_{k=1}^K p(\mathcal G_k \;|\; X) = 1

- f(X) = \argmin_{g\in G} \sum_{k=1}^KL(\mathcal G_k, g)p(\mathcal G_k \;|\; X)

- zero-one loss: f(X) = \argmax_{g\in G}p(g\;|\;X)

- f(X) = f_{bayes}(X)

- EPE(f_{bayes}) = E_{x,y}(L(Y,f_{bayes}(X)))

- E_{g|x}(L(G,\hat G(X))\;|\;X) =

\sum_{k=1}^KL(\mathcal G_k, f(X))p(\mathcal G_k \;|\; X)

Summary by Flavius Schmidt, ge83pux, 2025.

https://home.cit.tum.de/~scfl/

Images from Wikimedia.